Fidelity Bank – Wealth Management

January 2023

William J. Fennie III, CFA

Bond and Equity markets continued to rally in December as the Bloomberg US Aggregate Bond Index rose 3.83% and the S&P 500 rallied 4.54%. This positive momentum helped the indexes finish up 5.53% and 26.29% for the year, respectively. Cooling inflation driven by less robust employment demand, normalizing supply chains, and growing excitement that central banks will cut interest rates sooner in 2024 than previously expected propelled an ‘almost everything rally’ to end the year.

It is difficult to understate the importance of long-term investors to be invested during furious market rallies like we saw in November and December. August, September, and October were difficult months for stock and bond investors alike as the S&P 500 fell 8.25% and the Bloomberg Aggregate Bond Index fell 4.69%.

We had many conversations with our clients about navigating these difficult market environments and staying aligned with their long-term goals and objectives. If an investor pulled his or her stock or bond investment on 10/31/2023, the year-to-date returns would have been 10.69% for the stock investor (instead of 26.29%) and a loss of 2.77% for the bond investor (instead a positive 5.53%!).

What’s worse is now if that investor “wants to get back in” they are paying significantly higher prices for assets. As the saying goes, “sell low, buy high, repeat until broke.” Trying to time the market and missing the best days is a significant impediment to long-term investment success. As the worst days and the best days in the market tend to happen very close together, harnessing market environments like November and December becomes crucial for effective long-term compounding.

Equity

December’s 4.54% return for the S&P 500 left the index higher by 26.29% on a year-to-date basis. However, despite what had been the case for much of 2023, U.S. large growth stocks trailed value during the month (+4.43% vs. +5.54%).

On a year-to-year basis, growth rebounded after a disastrous 2022, bounding higher by more than 42%, easily outperforming its value brethren (+11.46%) by 31.22%. Small Cap stocks rallied 16.93% in 2023, with more than 12.20% of that return coming in December alone.

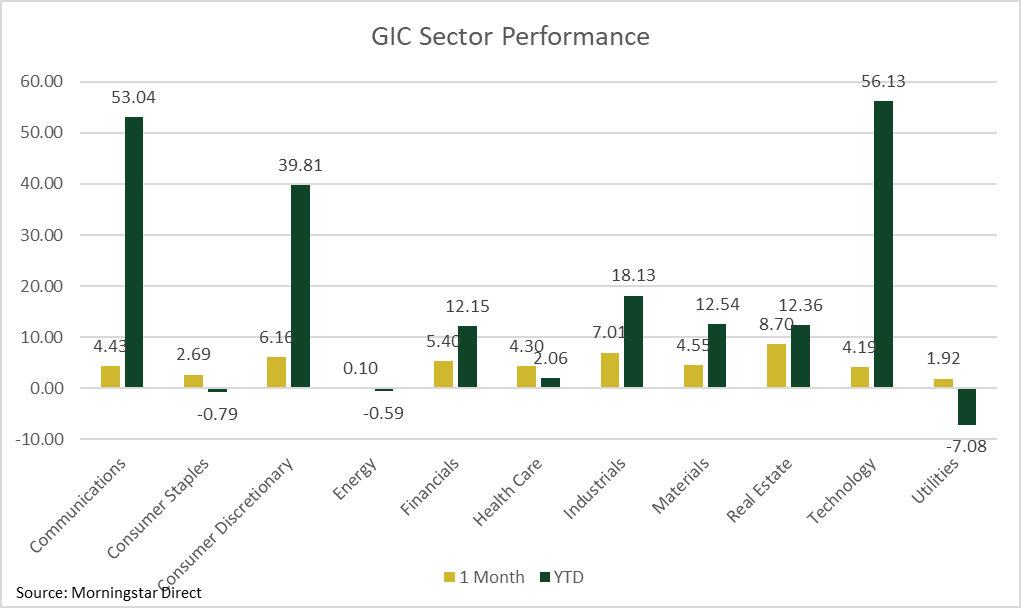

From a Sector perspective, Real Estate and Industrials were the best performing sectors with returns of 8.70% and 7.01% in December. However, year-to-date, Communication Services and Technology Sector were the top draw, returning 53.04% and 56.13%, respectively.

Non-U.S. equities were not left behind by December’s rally, with the MSCI EAFE gaining 5.31% and MSCI EM index advancing by 3.91%, both in dollar terms. Currency played a major role in the returns of both asset classes, as sharply lower interest rates in the U.S. detracted from the value of the greenback. Continuing from its November decline, the dollar fell by more than 2.00% versus the basket of developed currencies and by nearly 1.33% against the emerging basket in December.

Fixed Income

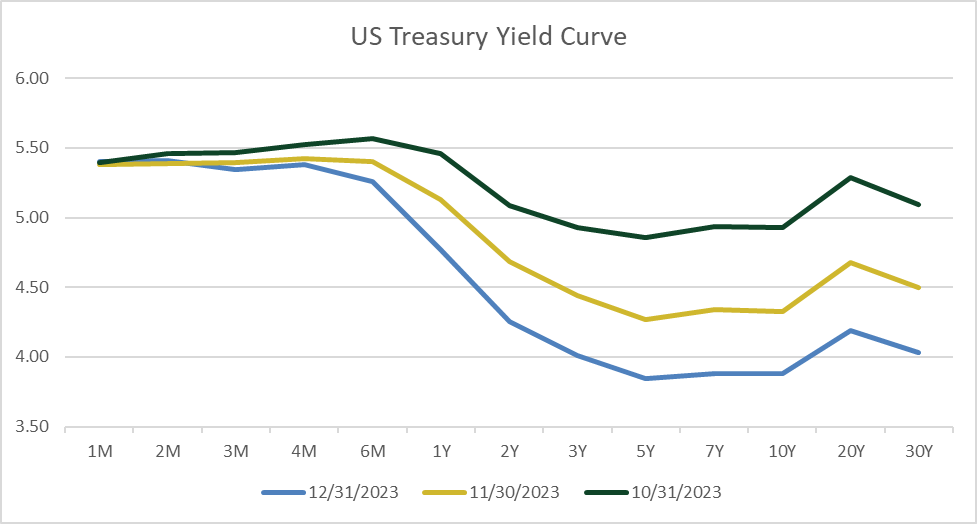

US Investment Grade Bond followed up November’s 4.53% gain, which was the largest monthly gain since May 1985, with a jump of 3.83%, which was the second largest monthly gain since May 1985! The rally has been largely fueled around the prospect of achieving a soft landing for the economy and that cooling inflation would impower the Federal Reserve to begin cutting interest rates sooner than anticipated. In fact, the Federal Funds futures market traders are pricing more than five rate cuts in 2024, starting in March. As such U.S. Treasury Yields continued to fall in December, falling more than 40 basis points at both the 10-year and 30-year points of the curve. Since October, 10- & 30-Year rates are down more than 105 basis points.

Real Assets

Broad-basket commodities were the exception to the “almost everything rally”. While industrial and precious metals locked gains on economic enthusiasm, declining rates, and a weaker dollar, the energy and agriculture complexes ended December broadly lower. Oil prices were choppy in December. WTI fell below $69 per barrel, then rose to more than $75, and then closed the year at $71.65. Lower rates helped breathe life into REITs as the asset class rose 17.98% in the 4th quarter, finishing the year up a positive 11.36%.

December 2023 Market Review is intended solely to report on various investment views held by Fidelity Deposit & Discount Bank and is distributed for informational and educational purposes only and is not intended to constitute legal, tax, accounting, or investment advice. Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. Fidelity Deposit & Discount Bank does not have any obligation to provide revised opinions in the event of changed circumstances. All data is provided by Bloomberg Finance, LP and Morningstar Direct. We believe the information provided here is reliable but should not be assumed to be accurate or complete. Data, if not otherwise noted, is as of 12/31/2023. References to specific securities, asset classes and financial markets are for illustrative purposes only and do not constitute a solicitation, offer or recommendation to purchase or sell a security. Past performance is no guarantee of future results. All investment strategies and investments involve risk of loss and nothing within this report should be construed as a guarantee of any specific outcome or profit. Investors should make their own investment decisions based on their specific investment objectives and financial circumstances and are encouraged to seek professional advice before making any decisions. Index performance does not reflect the deduction of any fees and expenses, and if deducted, performance would be reduced. Indexes are unmanaged and investors are not able to invest directly into any index. The S&P 500 Index is a market index generally considered representative of the stock market as a whole. The index focuses on the large‐cap segment of the U.S. equities market.

Fidelity Bank Wealth Management

101 N. Blakely St.

Dunmore, PA 18512

www.bankatfidelity.com

1-800-388-4380