Fidelity Bank – Wealth Management,

January 2024,

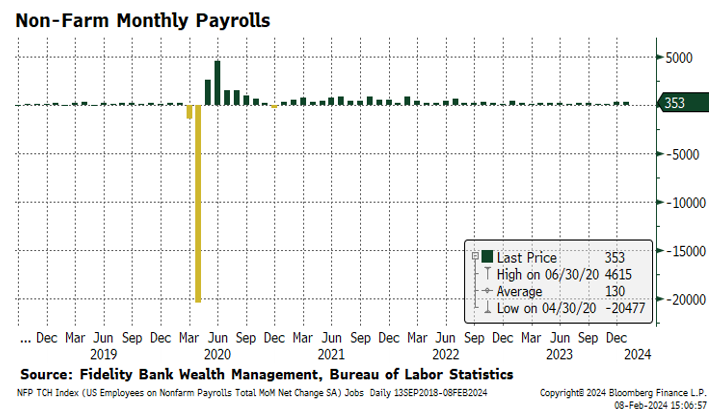

Global markets were a mixed bag to start the new year. After a rally in almost every asset class to end 2023, January saw US stocks rise 1.68%, while US Investment Grade Bonds fell 0.28%. Strength of the economy, inflation, disinflation, and the speed and timing of Federal Reserve shift in interest rate policy is driving markets on a day-to-day basis. Markets have been fixated on any clue as to when the Fed will lower interest rates. Unsurprisingly, the Fed left interest rates unchanged at its January meeting. Chairman Powell, in his press conference, also indicated that March is probably too soon for the Fed to start cutting rates. The January job report, released on 2/2/2024, indicated that 353,000 jobs were created in January, with upward revisions for December and November of 2023, highlighting a strong and resilient job market in the US economy.

Equity

The S&P 500’s march higher of 1.68% was led by High Quality Stocks (MSCI USA Quality: +3.13%) and Growth Stocks (Russell 1000 Growth: +2.49%).

Growth Stocks continued to lead Value Stocks in January, outperforming by 2.39% (2.49% vs. 0.10%). Small Cap stocks fell in January (-3.89%), mirroring the trend of Large Cap Stocks with Growth (-3.21%) outperforming Value Stocks (-4.54%).

From a sector perspective, Communication Services and Financials were the best-performing sectors with returns of 4.48% and 3.05% in December. Real Estate and Consumer Discretionary sectors were the laggards, falling 4.74% and 4.40% in January.

Developed Non-U.S. equities rose in January with MSCI EAFE gaining 2.61% in local currency and 0.58% in USD terms. While Emerging Markets lost ground in both local currency and USD terms, with the MSCI EM index falling by 3.49% and 4.64%, respectively.

Fixed Income

As the Federal Reserve has embarked on their hiking cycle, interest rate volatility has been the constant theme in the bond market for much of the past 2 years. Volatility as measured by the ICE BOA Move Index has largely remained above 100 since early 2022. Over the past year, the 10 Year Treasury Yield has risen from 3.30% to right around 5.00% to then fall to 3.80% and then ending January at 3.90%. As the Fed continues to evaluate its interest rate policy, it is likely bond market investors will have a bit of a bumpy ride; however, starting period yields are significantly higher than at the beginning of Fed’s hiking cycle. These higher yields should be a significant tailwind for bond investors as rates stabilize or fall in the future.

Real Assets

The Bloomberg Commodities Index was slightly positive by 0.40% in January as Oil prices (WTI) rose more than 7.70% as tensions in the Middle East put pressure on supplies. However, the industrial metals, the precious metals, and the agriculture complexes were all negative in January, falling 1.90%, 1.29%, and 1.03% respectively. After a significant rebound in November and December, REITs fell by almost 4.90% in January.

As global markets navigate various economic indicators and policy shifts, investors remain vigilant for cues amid changing landscapes.

January 2024 Market Review is intended solely to report on various investment views held by Fidelity Deposit & Discount Bank and is distributed for informational and educational purposes only and is not intended to constitute legal, tax, accounting, or investment advice. Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. Fidelity Deposit & Discount Bank does not have any obligation to provide revised opinions in the event of changed circumstances. All data is provided by Bloomberg Finance, LP and Morningstar Direct. We believe the information provided here is reliable but should not be assumed to be accurate or complete. Data, if not otherwise noted, is as of 1/31/2024. References to specific securities, asset classes and financial markets are for illustrative purposes only and do not constitute a solicitation, offer or recommendation to purchase or sell a security. Past performance is no guarantee of future results. All investment strategies and investments involve risk of loss and nothing within this report should be construed as a guarantee of any specific outcome or profit. Investors should make their own investment decisions based on their specific investment objectives and financial circumstances and are encouraged to seek professional advice before making any decisions. Index performance does not reflect the deduction of any fees and expenses, and if deducted, performance would be reduced. Indexes are unmanaged and investors are not able to invest directly into any index. The S&P 500 Index is a market index generally considered representative of the stock market as a whole. The index focuses on the large‐cap segment of the U.S. equities market.

Let’s get there, together.

Fidelity Bank Wealth Management

101 N. Blakely St.

Dunmore, PA 18512

www.bankatfidelity.com

1-800-388-4380